My retelling of the financial crisis and the recession requires some review of monetary policy, if for no other reason that the Fed frequently focused on housing during the crisis. Generally, individual sectors are only very selectively mentioned in FOMC statements. From May 2006 until recently, housing was mentioned in every FOMC statement except for October 2008:

May to August 2006:

Some version of:

Recent indicators suggest that economic growth is moderating from its quite strong pace earlier this year, partly reflecting a gradual cooling of the housing market and the lagged effects of increases in interest rates and energy prices.

September to December 2006:

Some version of:

Economic growth has slowed over the course of the year, partly reflecting a cooling of the housing market. .

January 2007

Recent indicators have suggested somewhat firmer economic growth, and some tentative signs of stabilization have appeared in the housing market.

March to June 2007:

Some version of:

...the adjustment in the housing sector is ongoing.

August to December 2007:

Some version of:

...the housing correction is ongoing

January to April 2008:

... deepening of the housing contraction...

June to September 2008:

...the ongoing housing contraction...

After that, housing was generally mentioned with regard to household wealth, housing starts, and the Fed's MBS purchases. Clearly housing was important, as it should have been.

Anyway, it bothers me a bit, because every Tom, Dick, and Harry, including those with much better credentials than me, has a criticism of the Fed, and I find most of those criticisms to be horrendously wrong. Why do I think I'm any different?

Yet, despite the fact that most everyone is wrong, the Fed is important. Actually, because most everyone is wrong, the Fed becomes important. What 'r ya gonna do?

I have recently been critical of rate hikes because of declining inflation and flatlined lending (although very recent bank real estate lending has

turned up). I fear the Fed Funds target is already pushing above a neutral level, and if that is the case, the Fed will certainly be too slow to reverse course.

And, I think this issue with the balance sheet will make it worse.

I really don't understand much of the academic treatment of Fed policy. I certainly could be wrong. I am not formally trained in these matters, so there is much I am certain to miss. Please correct me in the comments if you feel that I am wrong and salvageable.

Much of the treatment of Fed policy seems to treat long term rates as if they are simply a product of the sum of the intervening forward rates (that much is somewhat defensible) and that those intervening rates are purely a product of future Fed policy stances in a ceteris paribus world. It seems to me that more than even a few quarters forward, rates will be increasingly the product of factors out of the Fed's control or factors in the Fed's control that push rates in the opposite direction of short term Fed machinations.

Low long term rates were, famously, a "conundrum" for Fed officials in 2005-2006. The fact that they see this as a mystery seems like part of the problem to me. Policy rates during the time were basically neutral. There was no reason for forward rates to rise because expectations were muted. Far forward rates were actually

declining during the time. That's not because as the Fed was rapidly raising rates from 1% to 5.25% everyone was becoming convinced of their commitment to loose policy. It's because there was a sharp shift in sentiment, a massive buildup of savings, and a lack of risk-taking investment. Part of this is visible in sharply dropping housing starts and homeownership rates at the time. Yet, the Fed generally seems to have viewed those low rates as

stimulative.

The other thing I think is strange about reviews of monetary policy is that the liquidity effect seems to be treated as the overwhelming effect on interest rates. This is especially weird because these are extremely liquid markets. So, the idea generally seems to be that when the Fed loosens, it buys treasuries, which injects buying pressure into fixed income markets, pushing up prices. When the scale of these effects is measured, it seems to usually be done as a sort of event study. This is common in financial markets. But, that is because financial markets are generally perceived to be extremely liquid, with little

room for a liquidity effect. Prices shift immediately because future buying pressure is presumed as part of the current price. So, the effect of policy changes is measured by measuring the liquidity effect at the point of the shift. But, if the liquidity effect can be anticipated and priced by markets, then how can there be any liquidity effect at all?

So, my mind boggles when I see so many analyses of Fed policy that claim the QEs were effective because at the point of the policy shift, forward interest rates

declined. This is a backwards interpretation of the signal forward rates are giving, based on a signal that shouldn't exist.

Now, I must admit that in the very short term there does appear to frequently be a shift in long term rates in the same direction as a short term policy shift that doesn't really make sense if, say, loose policy signaled by lower short term rates should cause long term sentiment, inflation expectations, and therefore rates, to rise. I can't say forward rates confirm my complaints on a second-by-second basis.*

But, over longer periods, I don't see how these conventional versions of Fed policy review hold water. It seems clear to me that, as they were

implemented, the QEs were associated with rising long term rates, which then fell each time as QEs were terminated.

One of the great failures of my trading life was that I was set up with a position that was

highly sensitive to rising rates in the summer of 2013, and I managed to screw up the execution so badly that I ended up with nothing to show for it.

Anyway, what is odd to me is that conventional analysis of the QEs reverses this. So, unwinding the balance sheet is expected to

raise long term interest rates. Here is Gavyn Davies in the

Financial Times:

...the Fed will shed only around one third to one half of the assets it accumulated during the expansion phase, implying that the balance sheet will drop by $1.2-1.8 billion over several years. The total effect of this might be to increase 10 year bond yields by about 40-60 basis points...

The article later says:

Janet Yellen has suggested that the expectation of balance sheet normalisation has already increased the bond yield in 2017 by 15 basis points, which she says is equivalent to two 25 basis point increases in the fed funds rate. The market seems to think that the balance sheet run down will have an even larger effect on short rates than Yellen implies, which is perhaps why it is so reluctant to price in the full rise in rates implied by the FOMC’s “dot plot” for 2018-19.

So the liquidity effect, which must assume some sort of short term inefficiency in bond prices, has been anticipated. Rates have

already risen by 15 bp because spot prices reflect the inability of future spot prices to anticipate temporary shifts in Fed buying. (Please tell me how I have this wrong! I really would love to know that I am wrong.)

So, just because of institutional inertia, and the fact that rent inflation is wrongly attributed to monetary policy, I would expect the Fed to hold the Fed Funds Rate too high for too long, just like they did in 2007. But, here, we have an added problem. The expectation is that long term rates will rise as they unwind the balance sheet that was built up by the QEs. But, I don't think they will. As the program is implemented, long term rates will fall. Maybe not by much. But, I think they will fall a little bit. And, instead of seeing that as a problem, FOMC members will say, "Well, we were worried, because we thought unwinding the balance sheet would raise rates, but rates are falling. This will stimulate asset markets, which will allow us to continue raising rates."

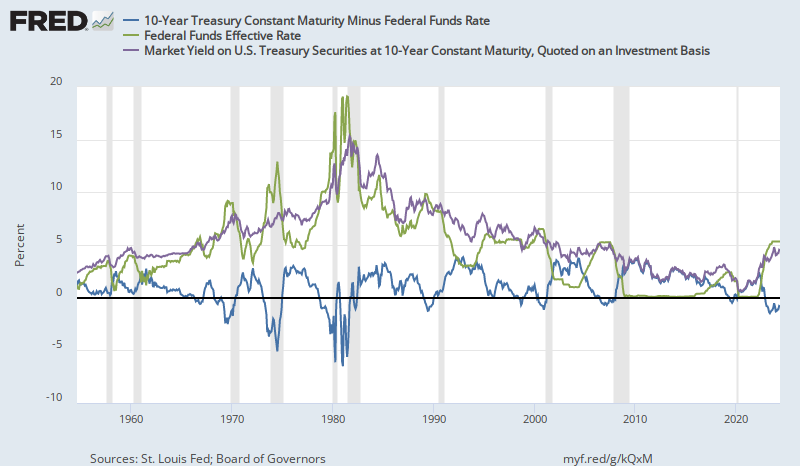

Of course, these events would lead to an inverted yield curve, which is a bad sign, and, according to

research at the New York Fed that I (and many other finance folks) do find useful, is associated with recessions (and, thus, declining interest rates).

Will the Fed raise rates as the yield curve starts to flatten? Surely they wouldn't, I want to think. But, there is 2006 and 2007. And, the consensus FOMC view seems to be that, if anything, rates should have risen higher and sooner.

This all is moving in slow motion, and there is some chance that some sort of economic momentum will outrun Fed tightening. So, this may come to pass in 2018, later, or never. But, it seems to me that a defensive posture is increasingly called for, and that, at some point, probably after another rate hike, a speculative position on sharply falling rates will be lucrative. I suppose, if I'm not crazy here, there is a variation on the old cliché at work. "The Fed can remain irrational longer than you can remain solvent." On the other hand, I generally prefer the corollary to that old cliché, which I heard someone say a while back. "The market can remain solvent longer than you can remain irrational." This probably describes the bulk of the speculative losses that have been excused by the original version of the cliche, and might also apply to mine. You should probably hope that's true.

* On the other hand, there are some pretty epic, and sort of funny, counter-examples in favor of the POV I am describing here. I remember hearing a press conference with Ben Bernanke in

June 2013, when, in response to the "taper tantrum" the Fed decided to promise to stretch out QE3 a little longer. He said, "These large and growing holdings will continue to put downward pressure on longer-term interest rates." Interest rates shot up literally as the words were coming out of his mouth. From the day before to the day after that FOMC meeting, the yield curve moved up about 40 basis points. Expectations destroyed the liquidity effect. To add a wrinkle to that, the move was effectively all in real rates - not in inflation expectations. The "taper tantrum" a month earlier had also been all in real rates. That might seem strange. But, when the primary effect of tightened monetary policy has been to collapse real investment, should we expect a reasonable loosening to be inflationary? I would like to attribute the May 2013 rise to improved real economic expectations, rather than to the proposed slowing of QE3, and the June rise to monetary accommodation. I realize that is a "just so" story. (Note,

however, that the rise in May was gradual while the rise in June was a sharp reaction to the FOMC meeting.) But, if you judge that, then you need a story that explains coherently how rates moved sharply higher as the Chair of the Fed explained that today's policy shift is intended to move rates lower.

The yield curve inversion remains in place. The curve as of Thursday looked very similar to the levels at the end of March and April. This seems to be a trading opportunity. I consider a yield curve to be a signal rather than a cause. During inversions, there is a bias in forward rates. Something keeps forward rates from moving as far below short term rates as they should, which means that there appears to be potentially persistent profit available by shorting forward rates when the yield curve is inverted.

The yield curve inversion remains in place. The curve as of Thursday looked very similar to the levels at the end of March and April. This seems to be a trading opportunity. I consider a yield curve to be a signal rather than a cause. During inversions, there is a bias in forward rates. Something keeps forward rates from moving as far below short term rates as they should, which means that there appears to be potentially persistent profit available by shorting forward rates when the yield curve is inverted. It seems like the trading position to take is to position for reversion while the Fed keeps the short term rate stable. Forward rates will move up and down within a range. Then, when the Fed moves the short term rate, forward rates will move out of the trading range. If it lowers the rate proactively, forward rates will move up. If it lowers the rate reactively, forward rates will move down.

It seems like the trading position to take is to position for reversion while the Fed keeps the short term rate stable. Forward rates will move up and down within a range. Then, when the Fed moves the short term rate, forward rates will move out of the trading range. If it lowers the rate proactively, forward rates will move up. If it lowers the rate reactively, forward rates will move down.