I fear I am entering curmudgeon territory, but there are just so many examples of wrong-headed thinking.

Here is an article at Slate:

"The Housing Industry Still Hasn’t Realized It’s Building Too Many Homes for Rich People"

That headline really tells you everything you need to know about what will follow, doesn't it? I mean, what sort of world does the author live in where he can imagine that an entire industry would not notice this?

"(T)his week, we got evidence that one of America’s largest industries may be running into trouble because its products appeal only to the upper crust."

"(W)ith each passing month, the homebuilding industry is pitching its products at a smaller, wealthier demographic slice."

Dozens, if not hundreds, of firms are constantly positioning in various niche markets to gain market share, and this just totally missed their attention. Where the industry had a massive decline in revenues so that they all continue to have difficult decisions about how much operational downsizing they need to do and where some have debt burdens that are still larger than their new smaller revenue base can support - so that practically any reasonable revenue growth would improve net profit margins - and, gosh darn it, they just can't get it through their thick skulls that there is a low tier market to serve out there. A market they were all happily serving 10 years ago.

Also, remember that in most cities, even though low tier markets never appreciated more than high tier markets during the boom, they have fallen behind high tier markets by 10% or more since 2008. If low tier markets were less profitable, one might expect builders to at least raise prices back to those previous relative levels. Strange that they would lower prices on those homes if the lack of profit is what drives this.

"There’s also evidence that existing homes (about 10 times more existing homes are sold each year than new homes) are getting too expensive for buyers."

One idea I hope to popularize is that we should think of affordable housing

consumption in terms of rent. Homes are getting too expensive because their rents are rising because we have broken the supply conduit.

"To their credit, in this expansion, the mortgage industry has not responded to the rising challenge of affordability by massively lowering its standards or by offering no-money down mortgages and other exotic lending instruments...Of course, there are a limited number of people in the U.S. who have $40,000 or $50,000 in cash lying around to make a down payment."

"Clearly, there is something of a housing shortage in the United States."

"The solution to the problem is for developers to increase the supply of affordable homes, and to bring large numbers of homes to the market that are closer in price to existing homes."

Come on, developers!

You're failing us! The solution to this problem is for you to provide supply for a market that we are determined to block funding for. This

your moral failing. Just one more piece of evidence of Wall Street screwing over Main Street. m'I right?

Of course, at the time I clicked on the article, the highlighted reader comment was:

"I would like to know more statistics about BUYERS in the past 5-10yrs. How many were American full-time residents and how many are foreigners, and of what class of dwelling?"

If there is anything worse than corporations, it's foreigners. They ruin everything.

The comments at articles like this offer an interesting peak at the fever dreams that drive policy today. There is one thing going on here - we have nearly universal support for obstructing access to mortgages compared to any previous modern standard - and this clearly has killed demand in entry level housing markets. This is the obvious reason for the shift in housing markets. There is nothing subtle about what has happened.

It's a little strange, because everyone that supports this shift should at least be able to come to terms with the effect it would have on the market. Instead of pretending this isn't a factor, they might say, "Well, homebuilders are only providing supply for top tier markets, but that makes sense, since we have shifted credit policy to decrease activity in lower tier markets." I think the core of the problem is that everyone thinks standards were sharply weakened during the boom and they have just gone back to normal. They don't realize that there was little shift in standards during the boom and the shift away from the norm has been during the bust.

Of course, recognizing that explains all of these mysteries about how the housing market has evolved since the crisis. But, people can't see it. So, this creates a sort of natural Rorschach test where they fill in the blanks with things that are wrong. There will always be some sort of perceived evidence in their favor. But, it is evidence that we know is not decisive because we know it is wrong. So, the reasons given - near-sighted builders, foreign buyers, a "rigged" economy, poor decisions of homebuyers, etc. give us a clue about what wrong reasons people are drawn to. They inevitably are about divisions, perceived inequity, in-groups and out-groups, corporate flaws, etc.

I think this is a reason why problems like this are so hard to solve, even if our chosen narrative villains didn't have anything to do with our original errors of judgment. Since our judgments weren't built on actual relevant facts, we end up filling in the holes in our narrative with our chosen villains. Once we do that, correcting to a more truthful narrative feels like it requires some sort of tribal disloyalty, because we filled the story with our tribe's mythology.

If you can talk yourself into believing that an industry that lost 3/4 of its revenue base has managed to err in leaving whole portions of the market untapped, then really, your narrative is flexible enough to accept any myths you may wish to attach to it. But, in the end, what choice would you have, if the world is aligned against uttering the truth?

(Another irony here is that the complaint about the pre-crisis market was how profitable it was to sell mortgages and homes to the low tier market. Everybody making bank on the backs of unsuspecting lower-middle class families. Now, I guess it's impossible to make profits on the low tier.)

-----------------------------

Here is an article at the Financial Times by columnist

Rana Foroohar. It is part of a series of posts where FT columnists point to important charts covering the past decade. Her chart shows that buybacks and dividends have roughly fallen and risen in proportion to equity values. And, interest rates have declined over the past decade.

That's the chart. I'm not sure how she expects dividends and buybacks to move relative to broader market levels, but she seems to think this is important. And, again, through some questionable assumptions about causation, we end up with a tale of dastardly corporations and a rigged economy.

As she tells it:

1) Loose monetary policy leads to low interest rates.

2) Low interest rates lead to binge borrowing by firms.

3) Firms use that cheap debt to buy back shares.

4) Share buy backs push up share prices.

5) This enriches the wealthy, since they own equities.

Let's accept #5. Numbers 1 through 4 are based on nothing. There is no mechanism through which the Fed could somehow be pushing long term interest rates well below the neutral rate for years on end. Monetary policy hasn't been loose, and if it had been, it wouldn't lead to a decade's worth of low long term interest rates. What were bond rates in 1979? This shouldn't be difficult.

Borrowing by firms isn't unusually high, either, in relation to enterprise value or to GDP. In nominal terms, levels get higher over time, though, so you can certainly make a graph that shows lines with positive slopes if you want to make this claim. One complaint about firms, to the contrary, has been that they are sitting on too much cash.

Total

payback ratios equity yields (dividends plus buybacks) have run around 5% of market value, plus or minus, for more than a century, and they continue to run at about that level. [edit: It appears to me that total payout ratios (dividends plus buybacks as a percentage of earnings) also tend to have a stationary long term mean level of about 60-70%.] Nothing unusual has been happening, except that regulatory changes in the 1980s led firms to shift some of this return from dividends to buybacks. If you want to know the reason for this, and you're having trouble getting to sleep, ask an accountant. It's not nearly as exciting as stories about "Wall Street" and "Main Street", though.

Using buybacks instead of dividends does raise share prices - or more precisely, dividends make share prices decline while buybacks don't. Basically, shareholders receive $1 in added share value instead of $1 in cash. But, there is nothing about buying back 2% or 3% of the equity stock each year that can, say, push prices up to 10% or 20% or 30% above some reasonable value they would have had otherwise.

So, a whole lot of nothing here is added up to create a story of an entire economic system rigged to benefit the elites at the expense of "Main St." And, this is from the Financial Times. Good grief.

Foroohar's book, alternately titled: "

Makers and Takers: The Rise of Finance and the Fall of American Business" or "Makers and Takers: How Wall Street Destroyed Main Street" has 4.4 out of 5 stars at Amazon. I'm sure it's a real page turner. Much more interesting than an accounting textbook about the arithmetic differences between buybacks and dividends.

Foroohar's narrative exists above the plane of empirics. The system is rigged. Wall Street got bailed out and Main Street didn't. How would you even address this claim, empirically? It can't be. It is simply a narrative construction and it is naturally satisfying enough that it can be filled with the detritus of our data filled age with little trouble.

-----------------------------

Here is even more

good stuff from FT. This time about housing in Silicon Valley. More rigged economy. Here, the sin committed by the dastardly firms is...brace yourself...growing businesses that provide many high paying jobs. I know. Corporations are the worst.

The entire article is about how these firms create pressures in the Silicon Valley housing market that make it hard for poor residents to remain.

It took a lawsuit from the city of East Palo Alto to get the social-networking company to consider ways to mitigate the effects of its whirlwind growth. The result was an $18.5m grant to build affordable housing for people on low incomes....

...“The narrative that has been preferred by these corporations is that it’s all because of their largesse. But they were coerced to the table,” says Romero. “When all is said and done, it doesn’t address one 150th of the impact that the size of these developments will have.”

Or, there is this:

The rent inflation is a symptom of the speculators who are pouring into the area to cash in on tech money.

So, I guess the reason Dallas has affordable housing is because they have more effective lawsuits against their local corporations? I guess, if it weren't for "speculators", those apartments would be renting for $600 a month? Dallas has fewer speculators?

Elsewhere, we have choice phrases like "Facebook and Google have shown themselves adept at buying up whatever dreams they haven’t been able to crush." and Google's headquarters "is spreading like a rash through Sunnyvale". "Instead of contributing to affordable housing, they 'don’t pay their fair share of taxes, they park the money overseas'." "These companies have a lot of capital that they could invest in affordable housing if they wanted to."

This article really lays it on thick. Here we have a case of firms that happen to operate in an industry that is geographically captured in some ways by an area with dysfunctional polities. To suggest that housing in Silicon Valley is a problem because Google and Facebook aren't as community oriented as, say, Delta Airlines or Home Depot are in Atlanta is bizarre. The companies have nothing to do with this problem. The article makes a brief reference to Prop. 13. But, it just keeps circling back to building resentment against these firms. In any functional city, does it even occur to people to think that employers are supposed to be actively involved in the local housing market? Yet, when politics leads to dysfunction, we seem to be naturally drawn to a certain type of narrative.

Imagine trying to get away with describing the expansion of any other group of people as "spreading like a rash". Economic rhetoric, especially since the housing bust, has been quite stark. When this sort of thing gets pointed out, it is common for people to react indignantly. Playing up wealthy corporations as victims is unseemly, isn't it?

When the medieval priest declared that local witchcraft was causing the outbreak of fevers, his solutions tended to be terrible for the local witches. But, you know who else the solution would be terrible for? The people with fevers! While our newspapers are filled with heated debates about the use of privileged language or ethnic and racial tensions, they are also filled with rhetoric that is sharply and obviously uncharitable to a predictable target. It's so strange that we can compartmentalize like that. I mean, even the language itself sometimes is quite parallel. How can we become more sensitive to it in some contexts and remain insensitive to it in other contexts. It regularly deposits scales over our eyes so that we don't notice the most obvious solutions to our problems. I mean, for anyone who just sits down and looks out at the world for a second, the idea that Silicon Valley housing is more of a mess than housing in Chicago is because Facebook isn't engaged enough with its community, or the idea that share buybacks have led to a rigged economy of haves and have nots, or the idea that homebuilders desperate for revenue are just leaving whole markets unmet - these ideas are nutty. I mean just fruit loops. I might forgive the guy at the end of the bar for thinking such things. He probably thinks I'm an idiot because I wouldn't know how to clean the valves on a '68 Mustang. There's a lot to know in the modern world. But, for cripes' sake, I'd like to think if he turned to the Financial Times, he'd have a chance at getting a little smarter about financial matters.

-----------------------------

One last one. Here is an

article about an affordable housing proposal in LA. The headline, "L.A. County’s Latest Solution to Homelessness Is a Test of Compassion" is a testament to our time. We don't need "tests of compassion". There is a vast realm of economic interaction and cooperation that might include compassion but doesn't require a super-human core of it at the visible center of everything we do. That is the realm of human action where most problems are solved. We have become so enamored with the more visible forms of compassion that exist on the edges of that vast realm, that we have ground the gears of progress and shared well-being to a halt.

So, LA has a homelessness problem, and they have this proposal to raise taxes and then pay individuals $75,000 if they will build an "affordable" backyard unit and rent it to a homeless or needy family.

According to the article:

On top of that, the county will also streamline the permitting process, an arguably attractive incentive considering that most of these “accessory dwelling units” in U.S. cities are illegal.

The article does mention that new laws at the state level might ease some of those restrictions. But, this is madness. It's illegal to just build these units with your own funds. If we rid ourselves of those types of restrictions, housing in LA would be affordable. Instead, LA is making an exception to those restrictions, but only limited to households who take public money to do it.

This makes sense when we understand that this is not really a solution. It's a test of our compassion. Private investors and speculators will not be a part of this process. That isn't the place they fill in our narratives of the time.

There used to be a time when American corporations made things. Today, they only serve as villains for our fever dreams. And, apparently, we'll have it no other way. That's not just a pithy aside. Think about the problems these articles are addressing. There are trillions of dollars' worth of benign economic transactions - the transactions that would naturally take place in an unfettered context - that would solve these problems. They don't happen because they are effectively illegal.

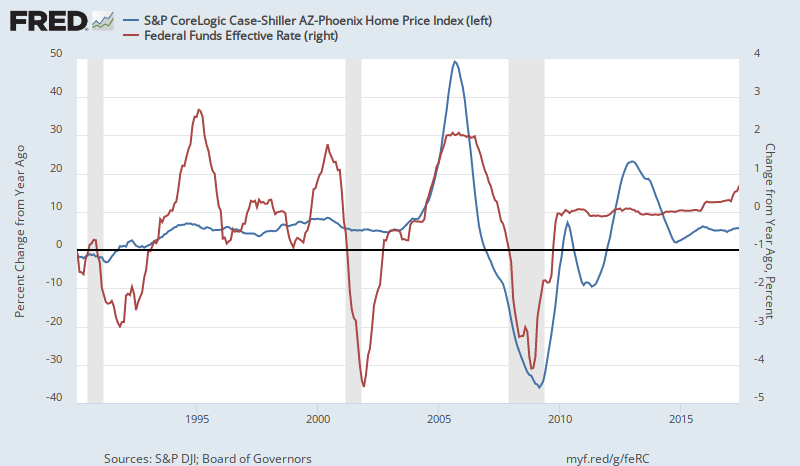

Bob thought this third graph was the best way to look at it - with the Fed Funds level and the change in prices. When prices were accelerating in 2005, rates were rising, but they were still relatively low compared to previous cycles, so they were still capable of fueling the bubble.

Bob thought this third graph was the best way to look at it - with the Fed Funds level and the change in prices. When prices were accelerating in 2005, rates were rising, but they were still relatively low compared to previous cycles, so they were still capable of fueling the bubble.