In yesterday's post, I considered housing subsidies as a sort of mandated annuity. Since tax benefits make homeownership more valuable, that value is naturally reflected in home prices. In housing, it appears plausible that in many areas, the value of those tax subsidies is so baked in to property prices that the typical buyer does not capture much net value. One sign of this is that tax subsidies don't seem to increase homeownership rates.

I suspect that the non-taxability of rental income for owner-occupiers is enough to tip the balance in favor of ownership for almost all households who would prefer it, and any additional benefits like the mortgage deduction or capital gains tax exemptions simply increase value for existing owners, and don't draw many new owners into the market. So, where those marginal effects take place, we find little effect on homeownership and almost total capitalization of the value into the price. But, in places like Germany and Switzerland, where they seem to really make an effort to eliminate all the tax benefits of ownership, homeownership rates do tend to run substantially lower.

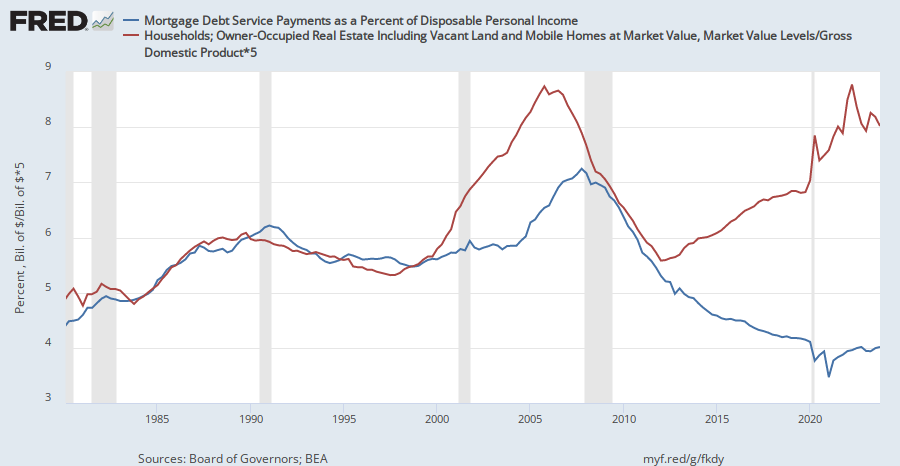

Currently, this is not the case in the US. Currently, homeowners are capturing a tremendous amount of economic rents, in terms of (rent/market price). According to national accounts data, net rental income on homes is running around 4% or more, after expenses and cost of capital. This is more than the nominal interest rates on mortgages, even before any capital gains on the property. If you can get a mortgage, you are practically guaranteed an abnormally high return on investment. That is because many households can't get mortgages. That is the only way to secure persistent economic rents - restrict access. This should be the number one rule of economics: you can't give something away without restricting access. Restricting access to mortgages has provided new homeowners with much more largesse than any tax subsidy ever did. (The largesse provided, or the cost imposed, falls on existing owners when these policies have been implemented. Homeowners unfortunately found this out during the crisis.)

Restricted access has lined the pockets of Closed Access real estate owners. It's the only thing that could have done that so thoroughly. This goes beyond residential housing. Every night on the local news in those cities are people righteously keeping out a Target because they like their local shops just fine, thank you very much, or keeping out a new pizza place because the powers that be decided there are already plenty of pizza places.

At any rate, the broader point this should cause us to think about is trust. A major problem with housing markets over the crisis period has been the volatility in both valuations and public policies. Reasonably qualified owners in 2006 - which includes just about all of them, even if being qualified doesn't get your story in documentary exposes of the "bubble" - lost months or years worth of income because credit markets and monetary policy were generous, then very not generous. Effectively, the rules of the game have been arbitrarily changed, and asset owners across the board had to roll with the outcomes. The peculiar trust of the market means that if our neighbors choose to frequent the new pizza place, we won't stop them. We have pre-committed to letting you fail. You can trust that. It is an incredibly important promise we have made. Even what looks like a communal act of support when we prevent our neighbors from trying the new pizza place is actually an abdication of trust. An abdication of trust that we would let our neighbors do as they please. An abdication of trust that we would allow new pizza parlors give it a shot. But, most importantly, an abdication of the promise that we would stand by and let your pizza parlor fail. That may be cold, but it's not nearly as cold as actively, communally undermining 20% of your homes value for your own good. Pre-committed neglect doesn't hold a candle to moral righteousness. Especially, when we can pre-commit to giving you support as you deal with your failure.

This undermining of trust is the case with any public policy. That is the point of public policy debates - that the rules are subject to change. Stability and trust are the key, illusive, features of a developed, equitable economy. When you buy a 30 year bond at 5%, the issuer of the bond can't call you up 5 years down the road and say, "Just wanted to let you know that we have had a change of ownership, and the new owners think 3% is a more reasonable rate." Trust is so key to a functioning economy. Much of public activism about economic fairness involves this ideal - that even if you have a powerful position, we communally demand that you do what you say you would do. Sometimes this plays out in civil or criminal enforcement, but the enforcement of these norms overwhelmingly happens informally in the natural evolution of private transactions.

We tend to think of trust as something that differs between honest, sincere actors and dishonest cheats. But, the housing bust is an unfortunately good example of how complicated trust is. There was near unanimity during the crisis that speculators and lenders needed to pay for what they had done. Many believed tight money, even at the expense of creating a financial panic, would impose discipline. Many have presumed that lower asset prices were the correct asset prices, so that household and financial balance sheets were decimated to suit our expectations. All of these economic dislocations were allowed or imposed with utmost righteousness. The mutual trust enforced by a market goes far beyond the enforcement of outright fraud. We are commonly the most morally confident about the worst things we do to each other. This isn't exactly a secret in human affairs.*

When thinking about public policy shifts, this is a real "elephant in the room" problem, I think. Trust is so important in private markets. And, when there is enough trust for those markets to function well, there is enough competition to generally pull average incomes and profits down to a level of indifference. Clearly, capitalists are continually working at developing little bits of monopoly power in order to capture excess profit. Comparing the P&Ls of 20 random small competitors in a competitive market will find much variation, with some owners doing very well. But, the market as a whole will reflect the best and the worst, and marginal new capital will expect only a reasonable return on investment, where entry is open.

The trust that must exist in those markets in order for profits to be bid down to levels of indifference does not exist in the realm of public policy. In fact, it cannot exist. That means that in contexts dominated by exposure to public policy shifts, we would expect incomes and profits to be excessive. If you are digging a new coal mine, and five years from now new laws limiting the use of coal may be passed, then you better have a high return on investment. In that case, this may seem like a good thing. The threat of changing rules would limit an activity that we might consider to be damaging, even if laws don't reflect that consideration yet. But, this is the case in every subsidy or tax. So, if there is a subsidy to benefit solar energy developers, but it is a subsidy that could be removed if the other party gains power, then firms built around capturing that subsidy will have to require excess profits to account for that risk.

Public policy that focuses on an active program of subsidies and taxes will inevitably lead to higher profits for those who are affected by them. This is systematically what we see in the comparison between developed economies, where rules are more stable, and developing economies, where they are not. This is what is problematic about corporate taxes that combine high rates with a myriad of deductions. This simply puts firms in a continual battle for the capture of economic rents, and a lack of access to those subsidies plus the instability of the rules means that firms tapping those rents will earn higher incomes. There is still open access to capital, in general, so that total capital income continues to claim about the same proportion of national income as it always has, but within the pool of invested capital, there seems to be an unusual amount of variance, with more winners and losers.

The difference between high trust private markets and public policy debates that erode trust is extreme.

The correct tax rate for incomes over $1 million is 100%, to raise no revenue at all. https://t.co/rcXKg03MEl— Marshall Steinbaum (@Econ_Marshall) October 30, 2017

In many cases, public policy is explicitly characterized as a way to change the rules specifically to harm others. My point here isn't to debate what the appropriate policy is. Inevitably, there will have to be some mixture of taxes and subsidies of various kinds. My point is to briefly pause and consider the shocking difference in our communal reaction to these two statements:

1) The head of Fidelity announces, "We have decided that 75% of all client income above $1 million will be confiscated."

2) Presidential candidate announces, "We believe that incomes above $1 million should be taxed at 75% to mitigate income inequality."

Again, the point here isn't to debate the policy. Some level of taxation is necessary. This debate must occur at some level. My point here is that trust is central to a functioning economy. It is so central that statement number 1 is beyond the pale. It is inconceivable. There is an informal, even unconscious, requirement for all the players in a functional economy to play by stable rules and to expect all others to do the same. We can palpably feel and understand the deep consequences of giving up that trust. The consequences are so severe that many actions that would undermine it aren't conceivable to us. There are less developed economies where something like that might occur, in large ways like the hypothetical above, or in many small ways (such as having strong norms for favoring family in business dealings or legal disputes, which extends to public officials). Those economies will not produce abundance until those universal trust expectations can develop. These are difficult problems to solve.

In our economic bubble, we take trust so much for granted that we don't even think about it. I liken this to my reaction to street vendors in Korea, who occasionally would simply have little boxes of currency sitting on a shelf, where patrons would place their payments, which could have easily been grabbed while the vendors were busy. I take that as a sign that, in some ways, South Korea has a higher level of social trust than we do. If I was a street vendor in the US, I wouldn't think of leaving that much cash sitting out. I suspect they can't imagine why I would worry about it. Trust is the water we are swimming in.

But, yet, in the political realm, we engage in trust-crippling actions and posturing as a matter of course. We must. There is no way around it. But there must be a tremendous amount of damage that this causes. We don't notice it because it is inevitable, just as we don't notice the many ways in which we trust agents in functioning markets because that is also inevitable. But, maybe occasionally we should make note of this cost to ourselves. What better day than Halloween? Maybe, tonight, I will dress up as macroprudential controls and roam the neighborhood correcting the misallocation of my neighbors' capital into candy. How else will they learn? Boo!

* CS Lewis: “Of all tyrannies, a tyranny sincerely exercised for the good of its victims may be the most oppressive. It would be better to live under robber barons than under omnipotent moral busybodies. The robber baron's cruelty may sometimes sleep, his cupidity may at some point be satiated; but those who torment us for our own good will torment us without end for they do so with the approval of their own conscience.”