They utilize longitudinal microdata to track the employment status of displaced workers over time. Using "non-employment" in lieu of "unemployment", they find little difference between the re-employment behavior of workers in the recent recession and workers of previous recessions. Here is a graph of very long term non-employment persistence from the paper. While there has been some change in the trend over time, there is little difference between recessionary times and expansionary times. Also, there is little difference between the outcomes since 2008 and previous periods. This is a fairly shocking finding, considering the well-known existence in the BLS's Household Survey of a large quantity of very-long-term unemployed workers.

They utilize longitudinal microdata to track the employment status of displaced workers over time. Using "non-employment" in lieu of "unemployment", they find little difference between the re-employment behavior of workers in the recent recession and workers of previous recessions. Here is a graph of very long term non-employment persistence from the paper. While there has been some change in the trend over time, there is little difference between recessionary times and expansionary times. Also, there is little difference between the outcomes since 2008 and previous periods. This is a fairly shocking finding, considering the well-known existence in the BLS's Household Survey of a large quantity of very-long-term unemployed workers. Here is a graph of unemployment duration by age. Keep in mind that short term unemployment durations are pretty normal now, so all of this extra average duration is coming from 1/6 of the pool of unemployed workers. So, estimating from BLS data, it looks like about 5.2% of the labor force is unemployed in a fairly normal labor market, with average unemployment durations of less than 20 weeks. Then, there is another 1% of the labor force that is unemployed, with an average unemployment duration of more than 120 weeks.

Here is a graph of unemployment duration by age. Keep in mind that short term unemployment durations are pretty normal now, so all of this extra average duration is coming from 1/6 of the pool of unemployed workers. So, estimating from BLS data, it looks like about 5.2% of the labor force is unemployed in a fairly normal labor market, with average unemployment durations of less than 20 weeks. Then, there is another 1% of the labor force that is unemployed, with an average unemployment duration of more than 120 weeks. At first glance, these data are telling two different stories. Here are some more graphs from the article. First, this graph shows the fraction of the labor force that has been non-employed for one year, two years, etc. This shows that extended unemployment was slightly worse in the 2008 recession than it had been in 1980, but not excessively worse.

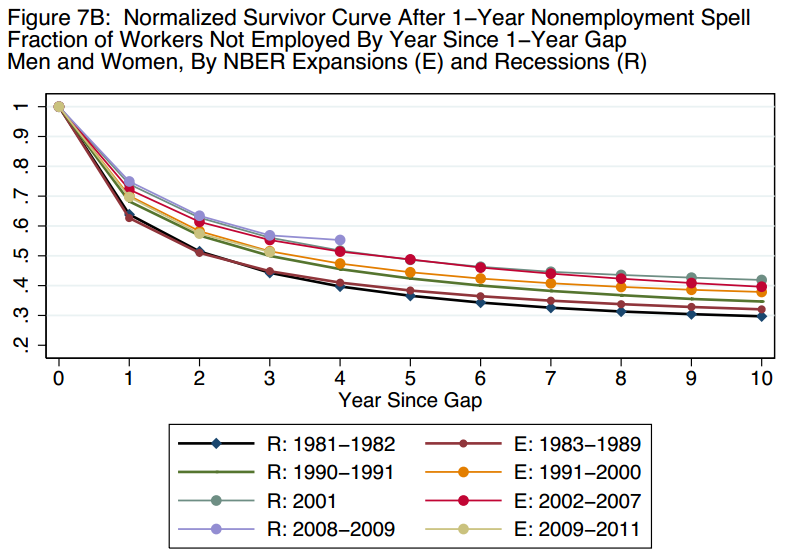

At first glance, these data are telling two different stories. Here are some more graphs from the article. First, this graph shows the fraction of the labor force that has been non-employed for one year, two years, etc. This shows that extended unemployment was slightly worse in the 2008 recession than it had been in 1980, but not excessively worse. The next graph (Figure 12A from the paper) shows the re-employment behavior of displaced workers in four recessions. The recovery to employment in the 2008 recession has followed a pattern similar to previous recessions. It is worth noting that a displacement episode appears to lead to a permanent 10% reduction in employment among the affected workers.

The next graph (Figure 12A from the paper) shows the re-employment behavior of displaced workers in four recessions. The recovery to employment in the 2008 recession has followed a pattern similar to previous recessions. It is worth noting that a displacement episode appears to lead to a permanent 10% reduction in employment among the affected workers.Finally, in the Figure 6A from the paper, we can see the surprising finding that the level of long-term nonemployment has been unusually low in the 2009-2011 period.

This suggests that much of the very long term unemployment in the current count is mostly a categorization issue related to workers whose behavior hasn't been materially different from previous recessions, but who may have been more likely to refer to themselves as unemployed in surveys because of subtle framing effects related to public labor policies, such as emergency unemployment insurance (EUI). If that is the case, it would suggest several implications:

This suggests that much of the very long term unemployment in the current count is mostly a categorization issue related to workers whose behavior hasn't been materially different from previous recessions, but who may have been more likely to refer to themselves as unemployed in surveys because of subtle framing effects related to public labor policies, such as emergency unemployment insurance (EUI). If that is the case, it would suggest several implications:1) Unemployment has been overstated, relative to previous recessions. This would apply to the approximately 1% of the labor force that currently is categorized as unemployed with very long unemployment durations. It would also apply to the U-6 unemployment rate that includes marginally attached and part time workers. The paper outlines how there tends to be marginal employment activity over time with long term non-employed workers, after a displacement, but that over time permanently non-employed workers become a larger proportion of the remaining non-employed. Following this pattern, we should continue to see a reduction in U-6 unemployment. I suppose that we might end up with a permanently self-identified population of unemployed workers, but I think it is more likely that to the extent that this group reflects the displaced workers who permanently leave the labor force, they will slowly begin to self-identify as not-in-the-labor-force.

So, if this is the case, the current unemployment rate, stated comparably to previous periods, might be in the low 5%s. This would explain how real wages have been higher than we should have expected, given the unemployment rate. The authors also point out that the permanently non-employed displaced workers tend to be older, which also might explain why unemployment in this recession tended to be excessively high for older age groups.

Here is a graph of employment flows. Note that the most unusual movement in the recent recession was the unusual increase in flows between unemployment and "Not in Labor Force". Flows between Employment and "Not in Labor Force" and between Employment and Unemployment reached levels slightly worse than the 2000 recession and about the same as the labor market in 1995 when these data series begin. And, these sets of flows are currently back at normal recovery levels. This would lead one to expect a business cycle where unemployment topped out in the high single digits and is back around 5%. The outlier here is the flows between unemployed and "Not in Labor Force", which moved much higher, relative to the other flow sets, and which remain elevated. Could this unusual movement reflect a change in self-identification and categorization among marginally attached workers who, in previous downturns, simply identified as "Not in Labor Force"?

Here is a graph of employment flows. Note that the most unusual movement in the recent recession was the unusual increase in flows between unemployment and "Not in Labor Force". Flows between Employment and "Not in Labor Force" and between Employment and Unemployment reached levels slightly worse than the 2000 recession and about the same as the labor market in 1995 when these data series begin. And, these sets of flows are currently back at normal recovery levels. This would lead one to expect a business cycle where unemployment topped out in the high single digits and is back around 5%. The outlier here is the flows between unemployed and "Not in Labor Force", which moved much higher, relative to the other flow sets, and which remain elevated. Could this unusual movement reflect a change in self-identification and categorization among marginally attached workers who, in previous downturns, simply identified as "Not in Labor Force"?This also comports with the recent high level of job openings and the idea that, adjusted for demographics, JOLTS indicators point to a historically comparable unemployment rate around 5.7 (which, given our current demographics would come in at around 5.3%).

2) I have been too hard on EUI. If this paper is on to something, then EUI didn't change labor behavior significantly, so it shouldn't be blamed for the long-term unemployment problem or for significant hysteresis in the labor market. These are workers who are mostly just being labeled differently within a fairly typical labor market behavior. I would still argue that it might not be the most efficient redistribution program, but this paper seems to support the argument that the apparent increase in unemployment durations from EUI comes mostly from movement between "Not in Labor Force" and Unemployment, not from delays in re-employment.

To the extent that this data is informative, it might suggest that in the next downturn, an extremely generous EUI program won't necessarily be that damaging to the labor market - it will just appear to be.

These implications would all generally point to a more optimistic picture of the current economic context. It would mean that historically comparable Labor Force Participation took a deeper cyclical dive than the reported numbers suggest. Although, the adjusted statistic would show a dip earlier in the recession, with stronger recovery since then. But, it also means that we are currently basically recovered and that the labor recovery was stronger and sooner than we thought it was. Much of the remaining reductions in unemployment would typically be recorded as re-entries into the labor force.

Finally, these findings show how beneficial functional NGDP targeting could be. There is something to be said for the creative destruction that might come out of a difficult economic period. But, I think it's incorrect to argue for unnecessary economic disruptions. The aggregate costs surely outweigh the benefits. This paper points to significant permanent disemployment coming from economic dislocations. If some of these labor disruptions are a result of suboptimal monetary policy, and if more stable nominal demand could prevent some of these dislocations, it could lead to higher labor force participation and utilization over time. I don't think higher labor force participation should be considered a goal, a priori. But, the permanent disemployment from these dislocations are almost certainly inefficient and are not remotely optimal for the affected workers, so in this case, it would represent improvement.