On a lesser scale, this could be happening again. There are slightly downward trends in both real GDP and inflation, and the Fed is talking about tapering QE. I'd say our best hope is that recovery continues strongly enough that interest rates rise on their own, with the Fed chasing them up when the time comes. We might extend the recovery for several years in that scenario. I'm afraid that the Fed will start tightening before that happens, and kill any nascent inflation, which is what we need in labor markets to counter the recent deflationary period and excessive inflation in non-wage compensation.

On the other hand, again, with the idea that reserves aren't that important any more as a banking constraint, maybe OMO aren't that important, and that limited banking capital is really all that's slowing down growth right now, especially with all the excess reserves in the system.

Maybe this will resolve itself if rates do ever move up, the propensity to hold cash decreases, and Fed assets lead more directly to increased currency, and inflation.

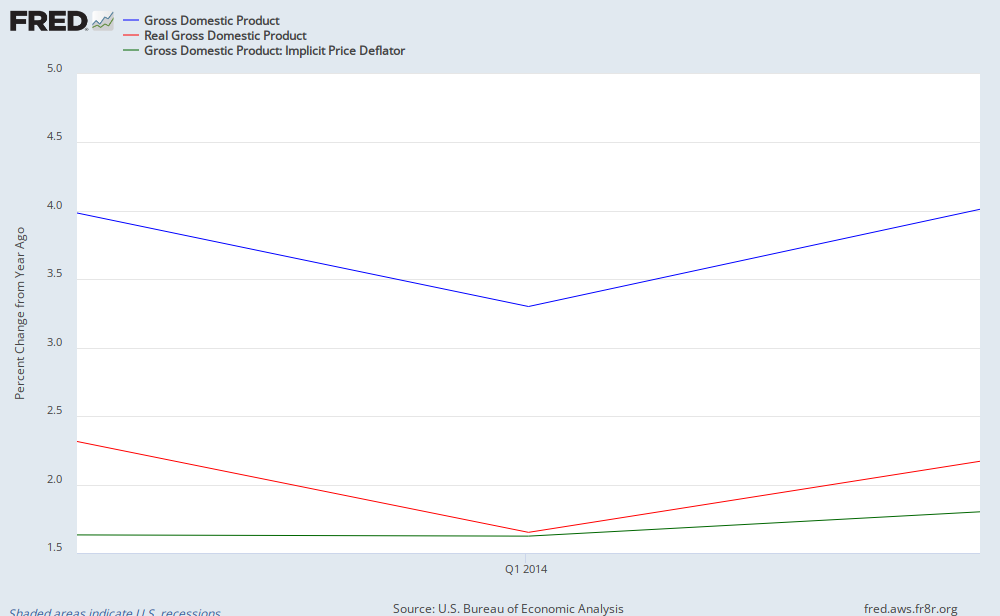

Boy, I'm confused. In any case, the graph below is not a sign of an effective Fed nor an inflationary Fed.

Addendum: Maybe the trend isn't so bad. Here is a graph of real GDP changes, comparing total GDP to private GDP (this has direct government purchases subtracted out, but still includes the effect of transfers):

The recent weakness in real GDP looks to be mostly a product of the reduction in federal spending. That is basically a one-time event that is finished, and the private sector seems to be growing at a somewhat decent rate, considering demographic headwinds. Maybe we can expect headline nominal and real GDP growth to kick it up a notch in the last half of the year.

Maybe we'll even see an uptick in the JOLTS data that has looked a little stagnant.

No comments:

Post a Comment