Inevitably, in a culture and an economy that exists above subsistence, saving is required. As abundance has grown over time, forms and outlets for saving and investment have become more complex. For any life more complex than hunting fruits and berries and killing small game, where nature's risks are always at the doorstep, speculation is mandatory. This is true for even the first steps into agriculture.

In our world, we are all involved in wild speculation. We have all optimized for a functional society with a complex array of utilities, public institutions, and market provision of highly technical goods. Frankly, it sort of stresses me out to think about it because we just aren't built to trust the robustness of emergent order, but we all must do just that, to an extreme. Mostly we cope by not thinking about it.

One of the ways we handle this unavoidable speculation is by engaging in a variety of risk-trading relationships, which, for the most part, settle into a set of social conventions that reflect common preferences, so we don't even think about it consciously most of the time. Local certainty appears to be very valuable. Much of finance involves trading local risk. Equity holders take on short term volatility and both creditors and laborers tend to accept a discount to their incomes in exchange for that certainty. This is why stocks generally have higher long term returns than bonds. It is difficult to be tethered to the random walk, both emotionally and as an input in our personal financial plans.

But, there is a necessary trade-off with these risk-trades. The gains in local certainty to laborers and creditors generally must come at the expense of more risks at the extreme. Equity is exposed to constant, small-scale local risk, and in extreme conditions may encounter existential risk. Labor and creditors experience this as a sort of regime shift. They either exist in a context of relative income certainty or in a context of default or unemployment.

Real estate holds an interesting position here. Mortgages with stable payments serve this function for both the borrower and the lender. Homes are real assets - their values change with inflation and with local conditions. Nominally fixed mortgages make a very poor asset-liability match. But, what mortgages provide for both the borrower and the lender is cash flow certainty. We use the general tendency for inflation, and amortization, to essentially push nominal uncertainty off the balance sheet of both the bank and the homeowner.

Note that both labor and creditors basically have made the same risk trade and face the same problems of dislocation when there are nominal spending shocks. But, isn't it interesting how different our reactions to these two classes of participants are?

Political observers and academics both tend to ascribe the causes of dislocations from nominal shocks to financial leverage. But, this is a truism. We are all speculators. We all optimize to some extent to our general expectations. One aspect of this optimization will always involve trading short term risk. If a nominal shock happens that is large enough to cause dislocation, it will, by definition, involve dislocation among these financial relationships that involve the purchase of short term certainty. To ascribe causality to debtors is equivalent to blaming the grass for a drought.

But, you may respond, some people get complacent and take too much risk. And those people are the ones that end up being the first dominoes to fall in a crisis. The causality is right there in front of our eyes to see. Is there any doubt that the housing crisis was heightened by the concentration of recent homebuyers with high leverage? Is there any doubt that the crisis would have been less severe with less leverage? No. There is no doubt. As far as it goes, this response is absolutely reasonable.

But, couldn't we also say that the drought would not have been so bad if the grass had deeper roots? Couldn't we also point to the clever means of water retention that desert plants use and wonder why the grass wasn't doing the same?

My point here is that even if the response is perfectly true, it is also not falsifiable. Any nominal shock that is strong enough to lead to widespread dislocations will appear to have been caused by leverage. Here is a post from the London School of Economics that explores the role of real estate speculation in the lead up to the Great Depression (HT: Benjamin Cole).

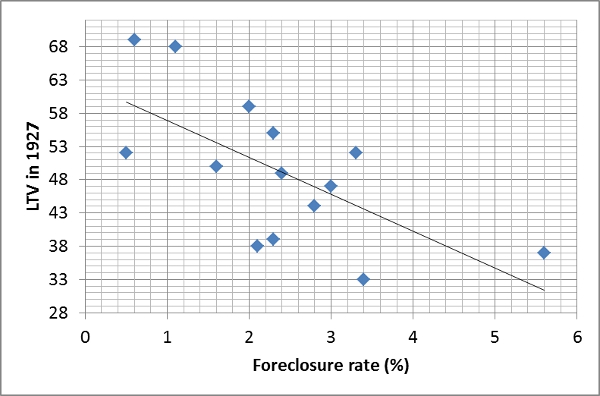

My point here is that even if the response is perfectly true, it is also not falsifiable. Any nominal shock that is strong enough to lead to widespread dislocations will appear to have been caused by leverage. Here is a post from the London School of Economics that explores the role of real estate speculation in the lead up to the Great Depression (HT: Benjamin Cole).Here is a graph from the post. The author, Natacha Postel-Vinay, makes some interesting observations about the real estate market of the time. In some ways there were parallels to the recent crisis. In the 1920s, piggyback loans began to gain popularity. This graph suggests a strange outcome, that in cities with lower 1st lien leverage, foreclosures were higher. She notes that this is because the lower leverage was associated with the use of piggyback loans, which were more vulnerable to economic stresses.

But, note, loan to values on first mortgages at the time were generally 50% or less. The cities with the highest foreclosure rates had LTVs under 40%. And, homeownership rates at the time were under 50%. Actually, even in the recent crisis, average leverage among homeowners was less than 50% at the peak of the boom in early 2006, though there were certainly cities with concentrations of higher leverage. So, if neighborhoods with LTVs above 80% or 90% were the cause of the recent crisis, would we have been better with LTVs under 80%, 70%, 60%? Certainly we would have been less vulnerable to dislocation. But, when dislocation came, would the story have changed? If average LTVs in 2006 had been 30% or 40% instead of 45% or if there was a ban on mortgages with LTVs above 90% or 95%, then when dislocation arrived, would we have said, "Well, we can't blame leverage this time."? Of course not.

And, note what we never claim. We never apply this prescription to labor. Even though the consensus among economists is strong that the difficulty for nominal wages to adjust downward is an important factor in episodes of unemployment, there is never an upswelling of academic papers and political candidates after a crisis that complain about our dangerous tendency to have labor contracts with stable wage levels. We never complain that our unemployment comes from a rigged system where so many laborers recklessly pushed up the operational leverage of firms. Nobody holds press conferences to complain that fixed-salary workers did this to us and bemoan that none have been prosecuted.

Yet, is there any doubt that if we instituted a law that required all labor contracts pay into a rainy day fund that firms could reclaim during nominal shocks that unemployment would be much less of a problem? How reckless of us not to do that! Maybe nominal crises are caused because laborers become complacent when there are long periods of stability. Maybe appropriate public policy should aim to allow frequent employment shocks so laborers don't get complacent.

Funny how that sounds wrong, even though it is basically the same proscription that is seriously offered in the financial realm. Operating leverage and financial leverage are both leverage.

Is there a façade of empiricism here? Do our shared notions about the causes of economic shocks exist in a plane above and disconnected from empiricism? Are we simply projecting our human biases in a subconsciously predetermined narrative?

If leverage is dangerous, the way to reduce it over the long term isn't through cyclical second-guessing. Corporate leverage has actually been very low going into the last two contractions. The reason leverage in general, by some measures, was too high was because low interest rates and supply constraints in housing had increased the value of homes. But, low long term interest rates are hardly a sign of speculative fervor.

|

| Source |

There were observers complaining about housing bubbles as early as 2001 or 2002. But, even when the crisis hit, aggregate home prices never fell below the prices of 2003. Suppose we had introduced enough nominal instability in 2003 to cause home prices then to fall back to 2001 prices. Would the story have changed? Millions of mortgages originated in 2003 and 2004 had low default rates. But, in this scenario, many would have defaulted. Is there any question about where the blame for the instability would have been laid? There is no question. We would have blamed debt and speculation. Yet, we know that there was nothing wrong with those mortgages. They have performed quite well, even though those 2004 cohorts have dealt with volatility unheard of since the Great Depression.

Nice post. I like the idea of building housing in high-priced areas. Now there is a topic that will never see the light of day.

ReplyDeleteI haven't seen concrete statistics but it seems to me that many, many more jobs are "equity-like" nowadays than in the past. Many people work for a bonus, or on commission, or have an element of company stock as pay. Granted, we haven't fully "equitized" compensation but we've made a lot more progress than we have in housing.

ReplyDeleteHm. I wonder. On the one hand, I do think we sort of had recessionary conditions by late 2006, and that unemployment was an especially lagging indicator, partly because rising costs were at the core of the problem, so the sticky wage problem didn't become operable until 2008. But, on the other hand, it seems to me that compensation and wages were especially sticky once we got to 2008 and that part of the problem with the long recovery was that wage growth was unusually high in 2008 and 2009, given the level of unemployment.

DeleteI mention Kevin Erdmann in the latest Historinhas post.

ReplyDeleteA very good resource for everybody that wants to read a good blog.

ReplyDeletecurrency exchange

So, Kevin, it is clear that the Fed wanted to take down the commercial paper market which I assume was for lending subprime. Subprime was crushed starting in late 2007 according to the commercial paper FRED chart here: http://www.talkmarkets.com/content/economics--politics-education/the-fed-did-one-thing-right-in-the-great-recession-but-it-wasnt-enough?post=88334

ReplyDeleteBut Helocs continued until the middle of 2008. That was based on Henry Paulson's assumption that subprime was contained. Inflation was also steady through the middle of 2008 or so. So, the Fed thought subprime was contained, or at least that is what they told everyone. Either they were incompetent or they crashed things on purpose because they saw the commercial paper market crashing and didn't lift a finger, just like they saw the LIBOR rate exploding and didn't lift a finger.

And I think there is proof that they allowed unacceptable risk in the CP market, and regulators knew about it, and were culpable for behavior that would be criminal if anyone else did it: http://www.talkmarkets.com/content/bonds/proof-the-federal-reserve-was-responsible-for-the-housing-bubble-and-crash?post=89477

Deletehttp://www.citylab.com/work/2016/03/map-geography-america-entrepreneurship-startups/474597/

ReplyDeleteInteresting, huh? So do constricted housing policies and entrepreneurial development somehow correlate with some other factor, or are entrepreneurial industries somehow drawn to cities with limited labor access in some sort of emergent process that limits competitive pressure?

DeleteWell, I think in simple terms.

Delete1. People like to live in nice places.

2. People perceive the glamor cities as more interesting and nice than Buffalo or the Inland Empire.

3. Tech companies are not limited by infrastructure as to location. They do not have to be near ports, or oilfields etc. So, they choose glamor cities for location.

4. Tech companies can hold down costs by jamming people into office space, even "creative" space (old factories). So office rents are not a barrier. Even some telecommuting.

5. There is some sui generis going on. The Hewlett Packard started Silicon Valley story, and Hollywood started in L.A., and some tech too (aerospace days). Wall Street in NYC. Harvard-MIT-Boston. Some of this was historical chance. Cleveland was strong in chemicals, but that did not generate spin-offs, at least that I know of. (BTW, I think there is history somewhere about the "high-tech" of each era moving west from the original tech capital, Troy NY).

My take is tech businesses in glamor cities are overcoming horrible restrictive selfish zoning, not abetted by it. U.S. glamor cities have not been investing in infrastructure, so the roads are so jammed in L.A. that every chance voters have they vote to block new buildings. Property owners probably sense scarcity works for their own property value. Americans have come to regard the virtues of single-family detached neighborhoods, and even minimum acreage requirements, as trumping free markets. Others hold sacred the character of their neighborhoods, the 1940s architecture etc.

By now, the demand for housing in glamor cities is so intense, that communities or towns in and around glamor areas know if they unzoned, there would be a tidal wave of community-crushing development in their city or town or neighborhood.

In Los Angeles, a forest of high-rise condos would line the ocean and in about a mile.

I think the solution is very, very unlikely, and that would be a reversal of the 1926 Supreme Court decision that legalized state and local property zoning.

One solution has been the emergence of Austin TX as another glamor city. If the US can develop five or 10 more glamor cities, that would help. Hey-hey Milwaukee! Yabba-dabba-doo!

I am surprised Hawaii has not emerged....

Interesting.

DeleteYou know, when I cast a wider net, the one additional city that shows up with the signatures of closed access is Honolulu.

"I think the solution is very, very unlikely, and that would be a reversal of the 1926 Supreme Court decision that legalized state and local property zoning."

DeleteThat still is not a solution if they don't fix the roads.

Gary--

DeleteIf there had been tremendous coastal density in California, then a subway system running more north-south would have emerged. I am mostly a free marketeer, but I recognize the need for government planning in infrastructure.

Re Honolulu: it has been years since I was on the island, but the last time I was there there was much talk about "overdevelopment" and saving Hawaii excetera. Later I was involved in a Hawaii housing development PR that had set aside for low-income people and so forth.

ReplyDeleteThe same old story: suffocate supply and then try to compensate.

Where is soaring global demand for housing in any place with a nice climate and safe government.

Thanks for this blog, I really enjoyed reading your post.

ReplyDeleteavast antivirus support phone number

yahoo mail customer support phone number

God is indeed a wonderful God,I want to share with you all that I was cared fully from my herpes infection after I got my herbal medicine from Dr Lucky..I will recommend who ever have herpes infection to contact or reach out to Dr lucky herbal medicine solution home because he have the strong herbal medicine for herpes infection. His Whats-app +2348154637647 . OR Email him via; drluckyherbalcure@gmail.com

ReplyDeleteThank you so much Dr Lucky for bringing my life back, i never thought i would ever be cured of HSV1 again due to the medical report i had from the hospital not until When God used Dr Lucky herbs and root in curing me of HSV1. Contact his on Email; drluckyherbalcure@gmail.com or WhatsApp him; +2348154637647

ReplyDelete