I think it is plausible that the housing supply problem that I have written so much about has been a key factor in recent business cycles. Note that in both 2000 and 2006, core inflation jumped up, but in both cases non-shelter core inflation was level and all of the marginal increase in core inflation came from shelter. In both cases, this was accompanied by a decline in housing starts - a very small one in 2000 and a large drop in 2006. In 2000, the Fed began lowering rates, and by the end of 2001, rent inflation began to moderate because supply had recovered. In the more recent episode, the Fed Funds rate was still holding steady at 5.25% in August 2007, after 18 months of a supply collapse. Shelter inflation began to moderate at the beginning of 2007, in spite of the supply collapse. Even before the Fed began to lower the Fed Funds rate, demand had been so undercut that housing consumption was decelerating more quickly than housing supply. The problem was so severe that neither housing supply nor shelter inflation began to recover until after QE was implemented.

I think it is plausible that the housing supply problem that I have written so much about has been a key factor in recent business cycles. Note that in both 2000 and 2006, core inflation jumped up, but in both cases non-shelter core inflation was level and all of the marginal increase in core inflation came from shelter. In both cases, this was accompanied by a decline in housing starts - a very small one in 2000 and a large drop in 2006. In 2000, the Fed began lowering rates, and by the end of 2001, rent inflation began to moderate because supply had recovered. In the more recent episode, the Fed Funds rate was still holding steady at 5.25% in August 2007, after 18 months of a supply collapse. Shelter inflation began to moderate at the beginning of 2007, in spite of the supply collapse. Even before the Fed began to lower the Fed Funds rate, demand had been so undercut that housing consumption was decelerating more quickly than housing supply. The problem was so severe that neither housing supply nor shelter inflation began to recover until after QE was implemented.

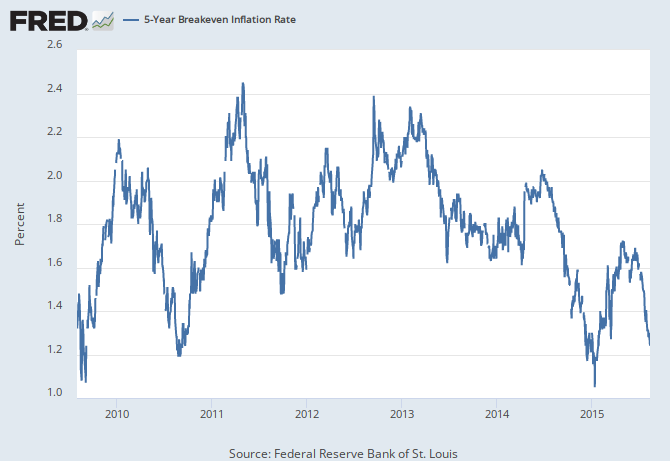

What's a little frightening about forward inflation expectations suggested by TIPS spreads is that the paltry 5 year breakeven CPI level of 1.2% includes shelter. Markets know that there is no reason for this rent inflation to subside, either because of our metropolitan housing policies or our financial "macroprudence", so this 5 year forward inflation expectation must reflect an expectation of non-shelter core inflation that is basically zero. The shelter inflation issue is structural. Forward bond markets are already predicting a monetary stagnation.

What's a little frightening about forward inflation expectations suggested by TIPS spreads is that the paltry 5 year breakeven CPI level of 1.2% includes shelter. Markets know that there is no reason for this rent inflation to subside, either because of our metropolitan housing policies or our financial "macroprudence", so this 5 year forward inflation expectation must reflect an expectation of non-shelter core inflation that is basically zero. The shelter inflation issue is structural. Forward bond markets are already predicting a monetary stagnation.

|

| Source |

If anything, the CPI measure of shelter inflation (which is mostly rent and imputed rent) is understating the current condition of the market. Here is a CNBC story that references Zillow's recent commentary on rising rents. The comments on that story are a great example of the sort of public sentiment that Fed decision makers must be facing. If housing prices are high, it's a bubble. If rents are high, it's a bubble. If the stock market rises moderately, it's a bubble. If wages rise, it's a bubble. Populists from all political factions seem to agree on these things, and that our only remedy is to suffer - as long as Wall Street suffers too. And, any monetary accommodation is seen as yet another Wall Street giveaway. If the bloodletting hasn't fixed this yet, what else can we do, really, but try another round?

(By the way, I consider the high quality of this blog's comments to be a minor miracle.)

I just returned from Seattle WA. An engineer buddy told me that there are NO high rise cranes to rent in the entire metro area and a lot of projects were waiting for construction equipment & crews to become available. So I asked what was being built. He replied, "Mostly commercial projects." When we talked about residential he said rents were increasing at a double digit rate. Then he said there was alot of discussion about "rent control" at both the city AND county governments. I said they should build more units. He told me they only build "upper bracket" units in the city center and the cheaper stuff "way out on the edges."

ReplyDeleteChilling discussion!

I was there a couple of months ago, and I noticed all the building downtown too. I had hoped it might be residential. Too bad. Sounds like they are going down the typical path.

DeleteYou know, regarding the cranes, I'm afraid that high density building has been stagnant for so long that we don't even have the network of suppliers and inputs that would be necessary to facilitate it if we ever solved the regulatory problem. I wonder how long it would take for feeder industries like the crane manufacturers to produce the physical capital it would take to have a functional metropolitan housing construction market.

DeleteI usually don't read the comments, so I don't know how good they are. But the posts themselves are great; they *ought to* attract good comments!

ReplyDeleteThanks, Philo!

Delete