Federal Reserve Chairwoman Janet Yellen said Wednesday it's possible the central bank might have needed to raise rates more quickly in the 2004-2006 period to prevent overheating in housing and financial markets. "Conceivably I think with the benefit of hindsight it might have been better to raise rates more rapidly or more during the 2004 to 2006 cycle.

You know, I'm not certain of that judgment but I think there is a case to be made." Ms. Yellen said during her press briefing.

That was a shift in tone for the chairwoman, who has previously dismissed claims that low interest rates helped fuel the housing bubble and subsequent crash.

By the end of 2006, the Fed Funds rate was 5.25%, the 10 year treasury rate was at 4.56%, and YOY currency growth was falling below 3%.

In the inflationary 1970s, forward rates would tend to rise along with short term rates. After the 1990 contraction, rates again followed the same pattern, but the upward movement during the recovery was weaker than the downward movement had been during the contraction. Inflation remained low as the yield curve flattened in the last half of the decade. But, after the 2000 contraction, while long term treasury rates began to rise, in anticipation of Fed rate hikes, the forward rates failed to show a consistent move upward. So, instead of seeing rates move up with the Fed Funds rate, across the yield curve, short term rates were moving up but long term forward rates were stagnant. By the time the Fed started moving the target rate up in 2004, forward rates were declining. As far as I can tell, there isn't a precedent for this. Forward inflation expectations were stable during this time. This was a decline in real long term forward rates.

I wish that forward rates were more commonly used and tracked. Looking at forward rates makes it much easier to separate long term expectations from the effects of short term target rate behavior.

My poor-man's estimate of the forward 7 to 10 year treasury rate in this Fred graph fell from 5.6% in June 2004 to 4.6% in February 2006, while the Fed Funds rate rose from 1% to 4.5%. All rates then moved together as the Fed Funds rate rose to 5.25% by July 2006, after which the yield curve inverted and 7 to 10 year rates fell back to around 4.6%.

|

| Source |

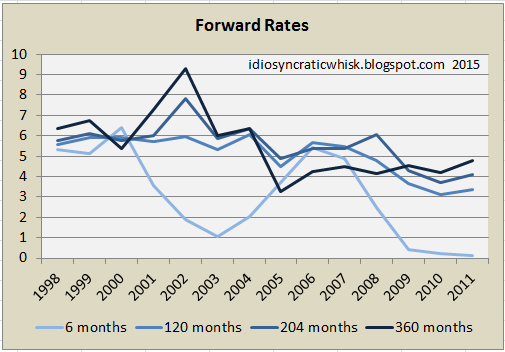

In the next graph, I have pulled future expected rates from the Office of Thrift Supervision Asset and Liability Price Tables , which I think are only available from 1997 to 2011. I have just shown the numbers here for June 30 of each year. (I included rates up to 360 months, but 30 year treasuries weren't issued from 2002 to 2005, so the 360 month number from those years may have a wider potential error.) This also shows falling forward rate trends for the entire period, including the period where the Fed Funds rate was rising and the Fed was supposedly dangerously accommodative.

In the next graph, I have pulled future expected rates from the Office of Thrift Supervision Asset and Liability Price Tables , which I think are only available from 1997 to 2011. I have just shown the numbers here for June 30 of each year. (I included rates up to 360 months, but 30 year treasuries weren't issued from 2002 to 2005, so the 360 month number from those years may have a wider potential error.) This also shows falling forward rate trends for the entire period, including the period where the Fed Funds rate was rising and the Fed was supposedly dangerously accommodative.As Scott Sumner points out, the Fed has just been following economic consensus, and in the quote above, we can see Yellen being pulled in this direction. Is there any basis for claiming that monetary policy is accommodative during a period where long term inflation expectations are level and forward real rates are declining? Yet this is what everyone claims. Even those who are with me in fingering monetary contraction as the cause of the financial crisis and most of the housing default crisis tend to accept that there was some period where the Fed was imprudently accommodative.

The singular source for this idea seems to be the strong price appreciation in housing. I had originally suggested that it was the long-running trend of tight monetary policy that had caused home prices to accelerate in the 2000s by pulling down long term interest rates. Low real long term rates were increasing the intrinsic value of the homes while low inflation expectations were lowering the monthly payment on mortgages and removing an obstacle to demand. During the housing "bubble", those real rates were probably mostly an exogenous factor, but at this point their continued decline is a product of market distortions coming from the crisis and disastrously tight policy.

But, as I have proceeded through my series on housing, I have been coming more to the point of view that our housing supply problem is mostly to blame. In this graph, I constructed a simple model of home prices based on actual rent inflation and interest rates, and compared that to counterfactuals with stable inflation and real interest rates.

But, as I have proceeded through my series on housing, I have been coming more to the point of view that our housing supply problem is mostly to blame. In this graph, I constructed a simple model of home prices based on actual rent inflation and interest rates, and compared that to counterfactuals with stable inflation and real interest rates.All the indexes begin in 1995 at around 80. In 2006, the Case-Shiller National Index had grown to 184 and the 10 city index had grown to 225. My modeled home price indexes (based only on rent levels, rent inflation, and real interest rates) tend to be a little noisier than the Case-Shiller indexes, and they come in a little low in 2006, at 173 and 196.

The counterfactual home price index with stable real interest rates and no excess rent inflation (rent inflation equal to core inflation ex. rent) rises to 99 in 2006, and the counterfactual that uses actual real interest rates but without the excess rent inflation rises to 116.

That suggests that only 1/4 of the price increases during the boom were related to low real interest rates. Three-quarters of the excess price increases, according to this model, were related to rent inflation - to the housing supply problem. (A small amount may also have been related to lower barriers to home buying demand because of the low inflation premium on mortgage payments, but I think this was small compared to the other effects.)

So, the housing supply problem has caused consensus demand for tight monetary policy because it has caused inflation to be higher due to persistent supply problems. But, indirectly, it has led to a consensus for tight money because of the tendency to blame the home price "bubble" on speculative demand. If the house price "bubble" was largely a supply phenomenon, the evidence overwhelmingly points to a general position of tight monetary policy throughout this period. As I have pointed out, Core CPI inflation less Shelter has been consistently below 2% since 1998. Currently Shelter inflation is running at 3% and Core minus Shelter inflation is at 1%, YOY.

Since the crisis, the low real rates that have been created by the crisis have become the overwhelming factor in pushing up the intrinsic value of the national housing stock. But, this is a disequilibrium. If we allow the home market to recover, rates will rise. The supply problem will not be solved, so the prices paid in the 2000s will be vindicated.

The question is, how many decades will it be before we stop calling it a bubble?

there have very authentic article about the basis of Housing Tax Policy From the Dow Jones news. such a important update to be share.

ReplyDeleteCapital gains tax un UK | Property Tax Clause 24 in UK

Mashreq bank UAE is provides the saving account opening in Dubai. That is provides the best account opening option in UAE and other Country.

ReplyDeleteIf you are a real player, then it is important for you to have in your life a lot of casinos in which it will be very easy for you to play and get as much pleasure as possible from the fact https://top-canadiancasinos.com/reviews/rizk-casino/ that you play in an online casino. You will easily spend time playing online casinos

ReplyDeleteIf you're interested in casinos and you live in Canada, you should definitely visit this site. It will really help you play cooler

ReplyDelete