There are several items I find interesting in this graph.

The Main Point:

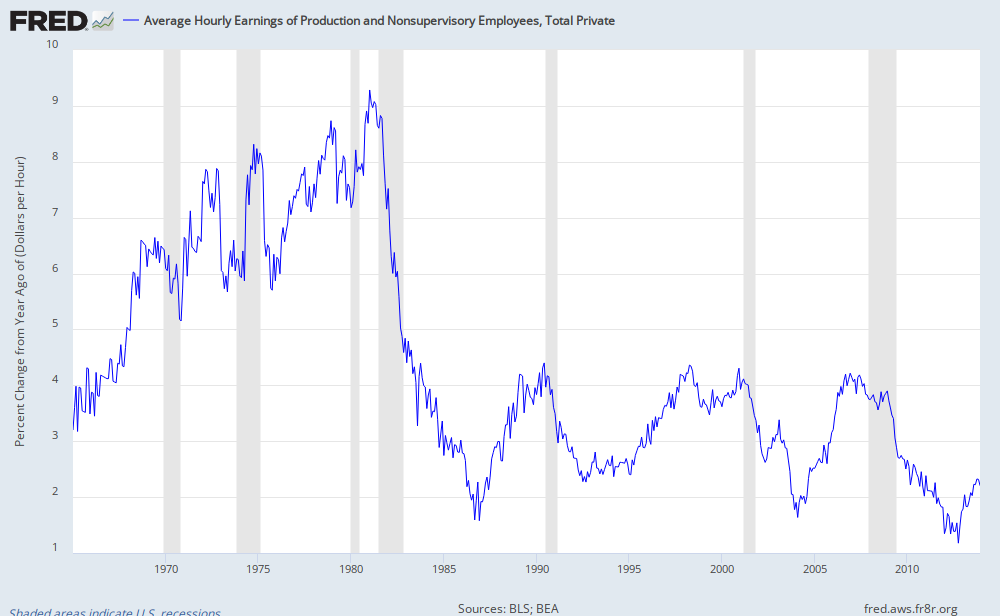

Nominal wage growth reflects inflation, which is really a reflection of Fed policy, and real wage growth, which is a reflection of the myriad of influences on labor markets. Wage growth is currently low, by historical standards:

This is mostly the product of tight Fed policy and low inflation. Since there is a widely held misperception that the Fed is being loose, I think this is a point that is being missed by most observers.

This is mostly the product of tight Fed policy and low inflation. Since there is a widely held misperception that the Fed is being loose, I think this is a point that is being missed by most observers.If we adjust for inflation, so that we are looking at real wage growth, we see that wage growth is quite strong.

That top graph reinforces my point that it is the unemployment rate that is giving us a false signal right now. Real wage growth this strong reflects a labor market that would normally be at 5%. If Congress doesn't reinstate EUI, I expect to see continued downward acceleration in the unemployment rate.

The question that remains is, will we see continued labor strength that pushes unemployment down to 5% in short order, or have there been a large enough number of frictions added to the labor market that unemployment will bottom out at 5.5% or 6%, like we saw in the 1970's.

Other Notes:

You can see the anomalous spike in real earnings growth in 2008. This is a sign of how badly the Fed messed up during that time. Late 2008 saw a deflationary collapse that doesn't show up anywhere else in the last 50 years' experience. (The other spikes in real wages were during expansions.) During this contraction, we were dealing with an unprecedented sticky wage issue, which has taken an excrutiatingly long time to work out of the system because the Fed has continued to keep inflation low.

It looks like, frequently, real wage growth spikes and then collapses in the period before a contraction. I don't quite understand the underlying factors there, but it shows up enough here to warrant a viewing when it becomes time to forecast the next contraction. It appears to be part of a pattern where nominal and real wages grow during the mature portion of the expansion, and as the next contraction approaches, nominal wage growth is mostly inflation-related.

PS: The PCE price index, less Energy and Food, appears to have the tightest pattern with the unemployment rate. Here is a scatterplot showing the correlation. The relationship has been tracking with the trend, but at an elevated unemployment rate. I think that gap will close after we normalize the unemployment insurance policy.

Considering that one of the contributing problems during shocks to the labor market is the tendency for wage rigidity to lead to unemployment, it is probably not a coincidence that a labor crisis that has been worse than usual has seen real wage growth at levels far above the trendline for the given unemployment level. Policies that have held wages too high have probably not been helpful in normalizing the economy. Deflation followed by an extended period of low inflation has worsened this problem. EUI worsened this problem.

The fact that real wages are trending higher suggests that much of the damage from tight monetary policy is a sunk cost at this point. If we can keep EUI from being reinstated, I will be watching to see if that helps get us most of the way back to normal. If the Fed stumbles into a moderate amount of inflation along the way, that probably wouldn't hurt, either.

|

| x=YOY growth in real wages (AHETPI/PCEPILFE) |

No comments:

Post a Comment