This labor report gave us everything we should want, and the unemployment rate even overcame last month's excessively low short-duration unemployment noise to tick down another tenth. This month saw a tick up in labor force participation and a large drop in "part-time for economic reasons", which has been slow in coming. There isn't much to be disappointed about in the household data. Yet, forward interest rates ticked

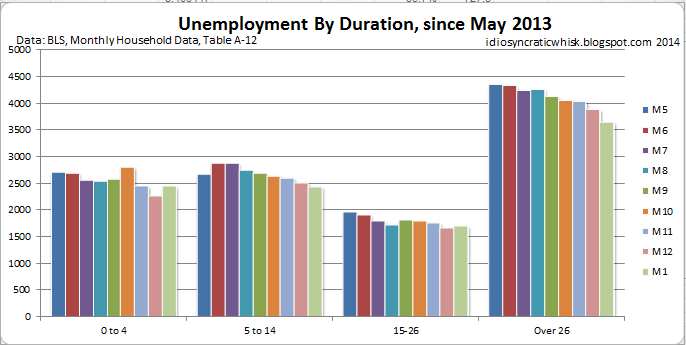

Here's an update on unemployment, by duration:

As I'd expected, the 0-4 duration unemployment from December wasn't sustainable. But, the numbers, in general, remained pretty low. We are starting to see an acceleration in the declining long duration unemployment levels. I had expected this also, and it is probably somewhat related to the end of emergency unemployment insurance.

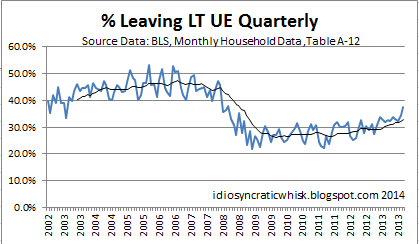

As I'd expected, the 0-4 duration unemployment from December wasn't sustainable. But, the numbers, in general, remained pretty low. We are starting to see an acceleration in the declining long duration unemployment levels. I had expected this also, and it is probably somewhat related to the end of emergency unemployment insurance. Here is a chart I have referenced before. This is a measure of how many workers who have been unemployed for more than 14 weeks exit unemployed status over the following 3 months. A healthy economy would see a level over 40%. This measure is up by 5% over the last two months, to 37.4%. If it hits 40% by March and 45% by June, we are probably looking at a 6% unemployment rate by June and a 5.5% rate by December. The recent post-EUI employment changes in North Carolina suggest that these projections are not out of line.

Here is a chart I have referenced before. This is a measure of how many workers who have been unemployed for more than 14 weeks exit unemployed status over the following 3 months. A healthy economy would see a level over 40%. This measure is up by 5% over the last two months, to 37.4%. If it hits 40% by March and 45% by June, we are probably looking at a 6% unemployment rate by June and a 5.5% rate by December. The recent post-EUI employment changes in North Carolina suggest that these projections are not out of line.There is this notion that transfers such as EUI create "multipliers". To me, it seems much more clear that there are multipliers from increasing employment. So, as former EUI recipients become re-employed, there will be complementary effects with the new production that do actually create a "multiplier". I would not be surprised to see a rebound in employment that exceeds the number of former EUI recipients. I think the over-under is that we shed another million from the "over 26 weeks" category by June. That is just as likely to be conservative as it is to be an overestimate.

PS. Average wages also look like they are continuing to accelerate.

PS. Average wages also look like they are continuing to accelerate.

No comments:

Post a Comment