Here, Jeff compares P/E ratios to 10 year treasury rates:

Here is a JP Morgan graph that Jeff references, on the correlation between weekly equity returns and 10 year treasury rate changes, at different rate levels:

At low 10 year rates, rising rates correlate with rising equities. This is despite the fact that low rates are associated with high P/E ratios. That relationship would suggest that rising rates would lead to lower P/E ratios, and hence lower prices, creating a negative correlation.

At high 10 year rates, the correlations work together - lower rates mean positive equity returns and higher P/E ratios.

This can be reconciled by the fact that high 10 year rates are the result of loose Fed policy. Inflation is the risk in this regime. Higher rates from higher inflation expecations mean higher risk, and thus, lower equity multiples.

A 5% rate on 10 year treasuries suggests a moderate Fed policy, where equity growth is dependent on non-monetary issues. The 1960's predates the two graphs above, but it was also a period with 4-5% rates on 10 year treasuries, high P/E ratios, and negligible correlation between equities and interest rate changes. This is roughly the rate area that market monetarists' 5% NGDP target would draw us to.

A low 10 year rate suggests monetary policy that is too tight. Here the relationship between P/E ratios and rates breaks down, since inflation is not significant in this context. Lower 10 year rates are the result of more tight monetary policy or negative economic developments, both of which are bearish developments for equities.

In fact, the top graph may show us a P/E ratio that tends to peak at 5-6% rates, falling at rates above and below that range, distributed with a positive skew. The JP Morgan graph is the first differential of that relationship, with a positive value below 5% and a negative value above 5%.

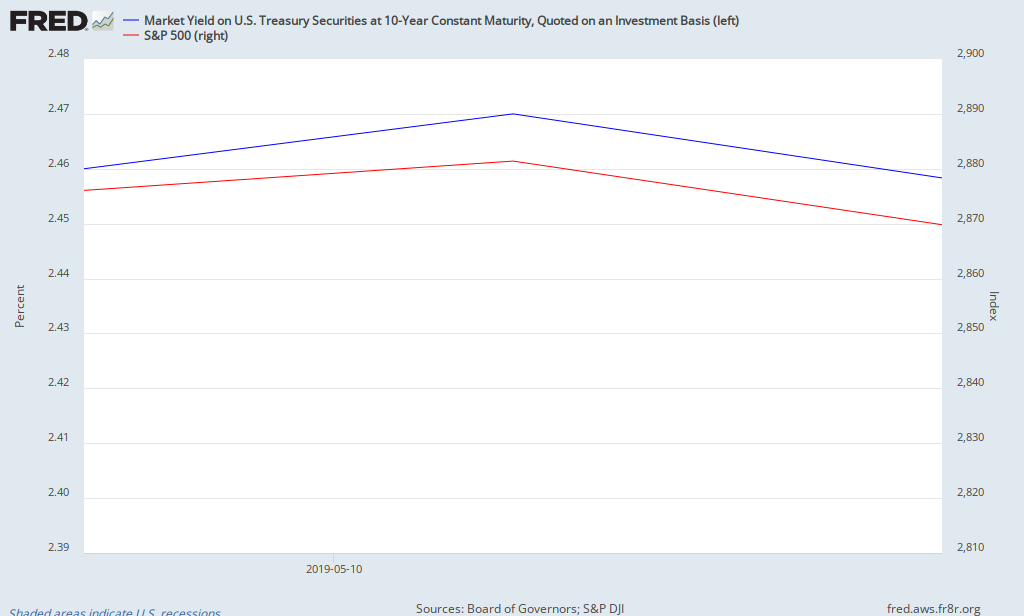

Market pundits who treat rising rates as a drag on the economy and on equity markets are operating with an incoherent model of how these markets interact. This appears to include pundits who are members of the Fed's FOMC. Here is recent S&P500 behavior compared to 10 year rates:

In June, the Fed announced a continued accommodative policy, which would only change if the economy continued to recover. With this comment:

Taken together, these actions should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative.Immediately, 10 year rates shot up 40 basis points. After a brief decline, equities continued climbing, also.

Elevate your wardrobe with apparel clothing from Izel Apparel, a brand known for refined style and quality craftsmanship. Each piece is thoughtfully designed to blend comfort, confidence, and contemporary fashion. Izel Apparel brings you versatile collections that celebrate individuality. Explore trend-forward women apparel curated to inspire your personal style. Shop the newest arrivals today.

ReplyDelete