Vince Foster has another intriguing post about Fed policy. It's another one where we come to the same conclusion, but with different priors. He is worried that the Fed will be too hawkish about pulling back on QE and cut off the legs of the recovery. I agree that, at this point, a hawkish error is more likely than a dovish error.

Along the way, he argues that the largest problem in 2008 was that the Fed allowed too much inflation. I think this is a good example where thinking in terms of interest rates can get us in trouble.

There is basically a Wizard of Oz problem with the Fed. The natural interest rate is a moving target, and in theory, if the Fed undershoots that target they cause inflation and if they overshoot it they cause deflation (or disinflation). The problem is that everyone assumes that all rates movements are Fed-led movements. I suspect that, at least over the last 10 years, the Fed has followed rates much more than they have led them. This is most obvious at times like in June, where the Fed announces that they are pushing rates down to continue to bolster the economy, and seconds after the announcement, rates shoot through the roof. This is a terrible problem, because if the Fed chases rates down, but everyone thinks they are leading rates down, we're all whistling past the graveyard.

And, this is where thinking like a market monetarist, which is the school of thought that says the Fed should target NGDP growth, can be illuminating.

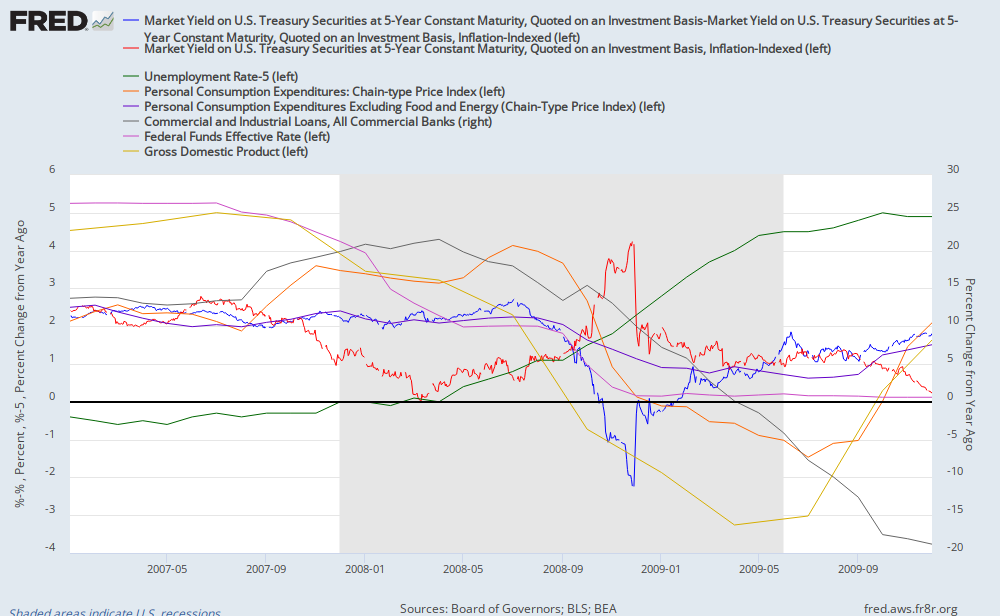

Here is a messy chart of the past decade, covering the period of time with TIPS spreads:

During the period coming out of the previous recession, from 2003 to 2006, the Fed is basically tracking the natural rate. The Fed Funds rate (pink) gradually rises into the recovery. Real 5 year rates (red) rise gradually also while 5 year expected inflation from TIPS spreads (blue) are basically flat. Excess unemployment (green), slowly declines, core inflation is tame (purple), commercial loans (gray) increase at a reasonable pace, and NGDP(yellow) first shows a snap back from the recession at up to 7%, gradually declining toward 5%.

First, I want to address this notion that the Fed overheated the economy. This assertion is based on one outcome - rising asset and home prices. As I outline here, home prices may have actually been stoked by a Fed that was too hawkish. And, in any case, this is a strange sort of amnesia. This obsession about the Fed and inflation is specifically a reaction to the 1970's, yet if one thinks about the 1970's, it should seem obvious that high inflation and loose money don't necessarily correlate well with high real economic growth, real asset prices, or with real stock market gains. There was a lot of stuff going on in the 70's (there always is), but I don't know of anyone who connects the extremely high inflation to an "overheated" economy.

But, back to the 2000's, up to 2006, all of these indicators seem very normal. The Fed was mainly staying out of the way. Even home prices were receding manageably in 2005 and 2006 as real interest rates climbed.

When 2007 hit, the interest rate interpretation of the Fed is that they started pushing rates down in order to stoke the economy, but inflation started to get out of control, and by the end of 2008, the housing bust, Bear Stearns, and Lehman were just too much for the economy to handle, so even when the Fed kept pushing rates down to unprecedented levels, it wasn't enough.

But, this all presupposes that the Fed is moving rates. Let's look at this from an NGDP perspective.

Here is a closer graph:

If the Fed was leading the way, we would expect a Fed Funds rate cut to cause a rise in some combination of inflation, expected inflation, and NGDP. Over the last half of 2007, coincident with minor cuts in the Fed Funds rate, we see steady inflation, steady expected inflation, and declining NGDP. In addition, the unemployment rate is starting to rise. To be sure, inflation with food and energy (orange) spikes, and commercial loans are still growing (this, though, is a lagging indicator).

But, the tricky part is the collapsing 5 year real rate. Interest rate based views of the Fed would attribute this to a liquidity effect, due to the Fed buying bonds in open market operations (which, by the way, they weren't, although their true effect on the money supply was muddied by the other liquidity operations they were providing to prop up the frozen mortgage-backed repo markets.). But, from an NGDP perspective, a collapsing real rate in the face of stable core and expected inflation, rising unemployment, and dropping NGDP growth is a good sign that the Fed is just chasing the rate down, and that trouble is brewing.

By summer 2008, while the Fed stubbornly held the Fed Funds rate at 2%, every indicator except the noisy inflation with energy and food measurement was heading in the wrong direction. Even the lagging indicator, commercial loans, was decelerating. By this time, even the rising real 5 year rate, coincident with a quickly rising unemployment rate, was probably an early sign of freezing credit markets.

The Fed didn't add liquidity to the market until QE 1 at the end of 2008. By then, fear and low rates meant the money supply would have to be bloated to unheard of levels to effect any inflation.

We are now, again, in dangerous territory. Since we are at the zero bound, the Fed isn't interest rate targeting, although they are still communicating through expectations of future rates. Recent rate increases are a good sign of economic prospects, similar to the rising real rates from 2004-2006, and unemployment should continue to trend down. But all inflation indicators are tame, and NGDP and commercial loan growth are anemic. We are again in a situation where a reversal of real rates is probably a bad sign. If falling real rates reflect new concerns about the economy, but they are interpreted as the result of Fed liquidity actions, we could suffer through more inappropriate hawkishness. Either NGDP, inflation, or real rates need to continue to show strength moving forward to support confidence in a continuing steady recovery.

As does Vince, I expect a continued recovery for the time being, but there is potential for money supply mismanagement here.

No comments:

Post a Comment